Introduction

Going to the dentist often feels less like a routine checkup and more like preparing for a financial surprise. Most people dread the thought of receiving a bill for a single filling or a root canal procedure. The cost of healthcare continues to rise faster than inflation rates in many sectors. Families are left scrambling to pay for unexpected oral surgeries or emergency visits. Without a safety net, these expenses can wipe out monthly savings budgets entirely. This reality makes securing proper coverage essential for long-term financial stability.

Dental insurance acts as a shield against these unpredictable costs. It is designed to help manage expenses related to cleanings, fillings, crowns, and implants. However, understanding exactly how these policies work can be confusing for the average consumer. Many people buy plans only to find out their favorite dentist does not accept them. Others discover waiting periods before they can access major restorative care. You deserve clarity before signing any contract or paying premiums.

This guide breaks down the intricate world of oral health coverage for you. We will explore different plan types, cost structures, and strategies to maximize your benefits. Real data shows that covered patients save hundreds of dollars annually compared to those paying out-of-pocket. Yet, finding the right balance between premium costs and coverage levels requires research. Whether you have an employer-sponsored plan or are buying individually, knowledge is power. Let’s walk through everything you need to know to protect your smile effectively.

Understanding the Fundamentals of Dental Coverage

Before picking a plan, you must grasp the basic mechanics of how dental insurance operates. Unlike medical insurance, which focuses on catastrophic events, dental plans prioritize maintenance and restoration. They usually operate on a percentage-based payment model rather than a flat reimbursement system. This structure means the insurer pays a portion while you pay the rest. Knowing these ratios helps you estimate costs before stepping into the office chair.

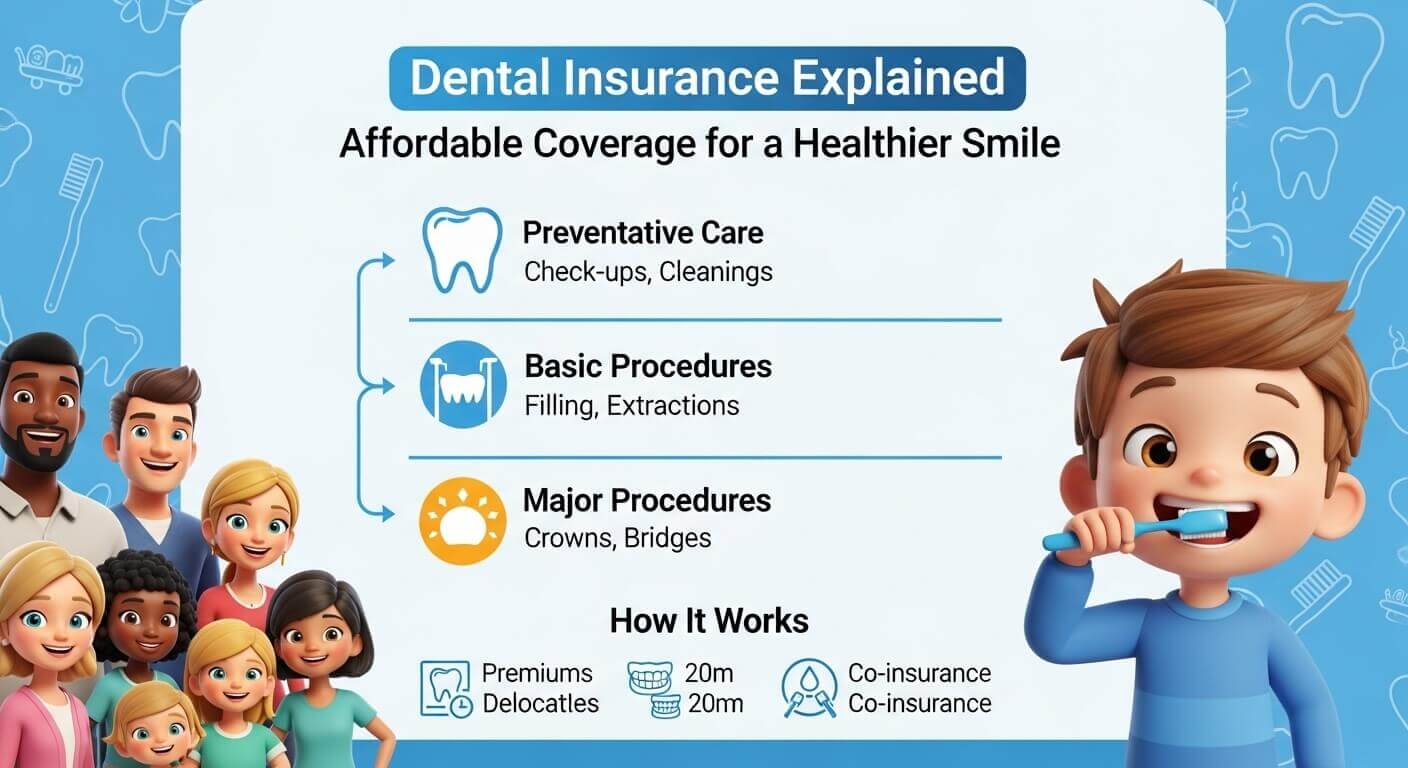

Coverage tiers typically categorize procedures into three distinct groups. Preventive care includes exams, X-rays, and cleanings performed twice a year. Basic restorative services cover simple fillings, extractions, and periodontal scaling. Major procedures encompass more invasive work like crowns, bridges, dentures, and root canals. Each tier carries different co-payment requirements and coverage percentages under most policies.

Popular Plan Structures and Networks

Most employers offer Preferred Provider Organization plans, or PPOs, to their staff members. These plans give you freedom to choose any dentist, though costs are lower if you stay in-network. You do not need a referral from a general practitioner to see a specialist in some cases. Premiums are generally higher for PPOs compared to other options available on the market. Flexibility often justifies the extra cost for families seeking a wide range of providers.

Health Maintenance Organization plans, or HMOs, restrict your choices to specific providers. You must select a primary care dentist from their approved list of professionals. Referrals are required to see specialists like orthodontists or oral surgeons within the system. These plans often have lower premiums but less flexibility when visiting clinics outside the network. Patients who stick to the network structure can save money significantly over the long run.

Indemnity plans are less common now but still exist for certain individuals. They reimburse you based on a reasonable and customary fee for treatments provided. You can visit any licensed dentist regardless of whether they belong to a network group. However, you usually pay upfront and wait for reimbursement checks to arrive later. Administrative hassles make these options less popular among modern consumers seeking convenience.

Coverage Limits and Service Exclusions

Every policy has an annual maximum limit on how much the insurer will pay in total. This cap often sits around fifteen hundred to two thousand dollars per person each year. Serious dental issues can easily exceed this threshold, leaving you responsible for the excess amount. High-risk patients needing extensive work might find these limits insufficient quickly. Understanding this ceiling prevents shock when bills arrive after big procedures.

Exclusions vary wildly between carriers and specific contract terms. Cosmetic procedures like teeth whitening are rarely covered under standard plans. Orthodontic braces often require a separate rider or a specific orthodontic-only benefit package. Some plans exclude services deemed experimental or investigational in nature. Reading the fine print regarding these exclusions saves money in the long term.

| Procedure Type | Typical Coverage % | Waiting Period |

|---|---|---|

| Exams/Cleanings | 80-100% | None |

| Fillings/X-Rays | 70-80% | 0-6 Months |

| Crowns/Bridges | 50% | 6-12 Months |

| Root Canals | 50% | 6-12 Months |

| Orthodontics | 50% | 12+ Months |

Breaking Down Costs and Hidden Fees

The sticker price of a treatment plan is not the only expense you will face. You must calculate deductibles, copayments, and coinsurance to get the true picture. Deductibles are the amount you must pay out-of-pocket before the insurance starts sharing costs. Some plans have low premiums but high deductibles that negate early savings. Paying this initial amount resets your clock for the year once met.

Copayments are fixed dollar amounts you pay for specific services at the time of service. For example, you might owe twenty dollars for a routine cleaning exam visit. Coinsurance is a percentage of the remaining balance you pay after the deductible is met. If a crown costs one thousand dollars and you have fifty percent coinsurance, you owe five hundred dollars. Understanding these terms helps budget accurately for upcoming appointments.

Managing Your Annual Maximum Wisely

The annual maximum is a hard cap set by your carrier on total payout amounts. Once you hit this limit, the insurance company stops paying anything for that calendar year. You would then bear one hundred percent of the cost for subsequent procedures until January resets. Scheduling major work early in the year allows you to utilize the full allowance effectively. Delaying expensive treatments until late December might mean paying full retail price.

Some plans carry over unused benefits to the next year, but this is rare for standard dental plans. Carryover provisions usually apply to flexible spending accounts rather than insurance contracts themselves. Be aware that using funds from a health savings account requires coordination with IRS rules. Do not assume leftover money rolls over automatically without checking your specific policy documents. Planning ensures you do not waste coverage potential annually.

Pre-existing Conditions and Enrollment Windows

Open enrollment periods dictate when you can sign up for new coverage without penalty. Missing these windows often forces you to wait for special life events like marriage or job change. Insurers view pre-existing conditions differently than they do in major medical insurance laws. They may charge higher premiums or impose waiting periods for specific treatments involving known issues. Disclosing history honestly avoids claim denials later on down the road.

Lapses in coverage can result in waiting periods even if you rejoin the same plan immediately. Continuous coverage maintains eligibility for faster access to major restorative work. Gaps allow insurers to classify previous work as new issues subject to waiting rules again. Maintaining uninterrupted payments is crucial for keeping your benefits active and robust. Always keep your contact info updated to receive renewal notices promptly.

Strategic Approaches to Selecting a Plan

Choosing the right dental insurance depends heavily on your current oral health status. If you anticipate needing significant work soon, look for a plan with fewer waiting periods. Families with children should prioritize pediatric coverage included in general adult packages. Individuals with excellent teeth might opt for a cheaper discount card instead of traditional insurance. Assessing your personal needs reduces unnecessary spending on unused benefits.

Employer-sponsored plans are often the most cost-effective option available to workers. Companies negotiate bulk rates with carriers that individuals cannot secure on their own. Even if you dislike a specific provider, the financial subsidy makes it worthwhile financially. You can often pick from a menu of plans tailored to different budget levels. Taking advantage of payroll deductions simplifies tax reporting and cash flow management.

Evaluating Individual Market Options

Buying a plan directly from an insurance carrier gives you full control over customization. You can shop online and compare quotes from multiple companies side-by-side instantly. State exchanges may offer subsidies depending on your income and family size eligibility. Comparing plans requires looking at both the premium and the potential out-of-pocket risk. Don’t forget to factor in travel needs if you move frequently within the country.

Some individual plans offer better network coverage for urban areas where specialists abound. Rural residents might find limited networks restricting access to endodontists or prosthodontists. Research local dentist directories included with each policy to verify provider availability. Call offices to confirm participation before submitting your application blindly. Verifying access prevents frustration when scheduling actual appointments for care.

Considering Alternative Benefit Models

Discount dental plans function differently from traditional insurance policies covering. They provide a network of participating dentists willing to offer reduced fees to members. You pay an annual membership fee but no premiums for individual claims processing. These plans can be cheaper overall if you rarely need extensive restorative work done. Membership cards grant immediate access to discounted pricing upon first visit.

Health Savings Accounts paired with high-deductible dental plans offer tax advantages. You contribute pre-tax money that grows tax-free until withdrawn for qualified expenses. Qualified withdrawals cover eligible dental costs, including vision, sometimes in broad categories. This setup appeals to healthy individuals who rarely need frequent dental procedures. Consult a tax professional to ensure compliance with IRS guidelines correctly.

Optimizing Your Benefits for Maximum Value

Maximizing returns on your dental investment requires strategic timing and organization. Many people wait until cavities turn into infections before seeking any kind of help. Utilizing preventive benefits annually keeps minor problems from becoming major repairs later. Cleaning twice a year is the best way to prevent gum disease progression significantly. Insurance covers most preventative care at one hundred percent under most plans.

Keep track of your claims history and appointment dates meticulously. A shared digital calendar helps coordinate family members across different schedules. Note expiration dates on treatment estimates before they become invalid. Estimates usually last thirty to ninety days, depending on the provider’s administrative policies. Submitting claims quickly avoids filing deadlines expiring accidentally during busy times.

Coordination Between Medical and Dental Policies

Sometimes oral health issues overlap with systemic medical conditions requiring dual coverage. Sleep apnea devices might fall under dental benefits, while respiratory equipment falls under medical. An injury resulting from an accident could trigger a medical insurance payment for dental work. Understanding how these policies coordinate prevents duplicate billing errors. Always inform both doctors about the existence of separate coverage for specific incidents.

Orthodontic work occasionally receives partial funding from medical plans if medically necessary. Jaw misalignment causing chronic pain might qualify for broader coverage eligibility. Documentation from a surgeon supports the medical necessity claim for such requests. Coordinating both sources can double the available funds for complex reconstructive surgery. Ask your case manager to assist with cross-referencing applicable benefits properly.

Network Verification Protocols

Always verify your dentist is in-network before booking any non-emergency appointment. Being out-of-network can increase your costs drastically beyond what you expected. Confirm their license status and address matches records held by your insurance carrier. Insurance portals update networks regularly, so assumptions can lead to surprises. Call the provider directly to cross-reference their participation status with the insurer website.

If a specialist charges above the usual and customary rate, request an itemized quote first. You might agree to pay the difference yourself if it fits within your budget constraints. Written estimates protect you from surprise balance bills after treatment concludes. Ask the front desk to submit a pre-treatment authorization form before proceeding. Approval numbers serve as proof of payment intent for financial clearance.

Common Errors That Inflate Healthcare Costs

Even savvy consumers make mistakes that drain savings unnecessarily throughout the year. Ignoring waiting periods leads to paying full price for procedures covered elsewhere later. Assuming cosmetic improvements like whitening are included wastes precious plan premiums. People often overlook that orthodontics requires separate funding buckets within standard plans. Checking exclusions carefully saves thousands of dollars over a lifetime of care.

Failing to verify coverage before treatment causes denial headaches later. Dentists sometimes submit claims assuming coverage exists without confirming specifics first. You could end up owing for a major surgery you thought was partially covered initially. Never proceed with expensive work without getting a clear explanation of benefits beforehand. Written confirmation shields you from disputes regarding policy language interpretation.

Neglecting Preventive Schedules and Reminders

Skipping scheduled cleanings accelerates decay rates and increases future repair costs significantly. Insurance rewards compliance by waiving copays for biannual maintenance visits. Skipping these sessions breaks the cycle of early detection and intervention effectively. Early cavity filling costs much less than full root canal therapy procedures. Regular visits build trust with hygienists who spot trouble spots immediately.

Forgetting to update your address or phone number delays critical communications from carriers. Missed renewal notices might leave you without coverage during peak illness seasons. Lapsed communication channels make resolving claims much harder when emergencies occur. Set automated reminders on your phone for open enrollment and appointment due dates. Staying proactive prevents administrative glitches from affecting your physical well-being being.

Misinterpreting Claim Denial Notices

Denials happen often due to coding errors or missing documentation submitted by providers. Understanding the reason code printed on the notice helps you fix the issue quickly. Appeals processes allow you to contest denials if you believe they were made in error. Providing additional clinical notes from your dentist strengthens your case for approval. Persistence pays off when fighting for rightful coverage under your contract terms.

Don’t accept the first denial without reviewing the supporting evidence provided by the insurer. Sometimes simple clerical mistakes cause rejections that auto-systems flag as invalid claims. Correcting codes and resubmitting fixes the problem without needing legal intervention. Keeping copies of all correspondence protects you during dispute resolution processes. Organized records make arguing against unjust denials easier for everyone involved.

Final Thoughts on Protecting Your Oral Health Investment

Securing reliable dental insurance is a smart move for anyone concerned about future costs. It transforms unpredictable expenses into manageable monthly payments spread over time. Prevention becomes affordable when coverage removes the barrier to entry for routine visits. Investing in your mouth invests in your overall systemic health and confidence. Small choices today determine your comfort levels years down the road significantly.

Knowledge empowers you to navigate complex insurance jargon with confidence and ease. Understanding terms like coinsurance and deductibles demystifies your billing statements completely. You stop fearing the unknown and start planning strategically for every checkup. Taking control of your coverage ensures you get the care you need without breaking the bank. Peace of mind comes from knowing your policy supports your health goals effectively.

The landscape of dental coverage changes constantly to reflect economic realities. Adapting to new regulations ensures your protection remains current and valid always. Stay informed about updates that affect your specific plan and provider network. Education remains your strongest tool against confusion and wasted financial resources. Choose wisely, read thoroughly, and enjoy a healthier smile for decades ahead.